Author: David Olnick, Investment Executive

Yesterday’s data on Producer Prices (PPI) came in sharply lower than had been anticipated. In addition to PPI, we also had data releases on Retail Sales and Industrial Production, both of those also coming in much weaker than had been anticipated.

Predictably, reaction in the bond market was swift with yields plunging and prices of bonds rising. Yields on 10 year treasury notes are now at their lowest level since last September near 3.40%. Even 2 year treasury notes, now near 4.10% appear to be discounting a possibility of rate CUTS in the not too distant future (perhaps late 2023/early 2024).

Early reaction in equities was positive since those were reacting to the decline in rates. However, once the short-sighted short-term traders realized the a deteriorating economy will negatively impact corporate earnings, the earlier buyers of stocks then reversed course and started selling. Currently the DOW JONES is lower by about 350 points.

On a positive note, weekly mortgage applications experienced a signification jump due to recently declining rates.

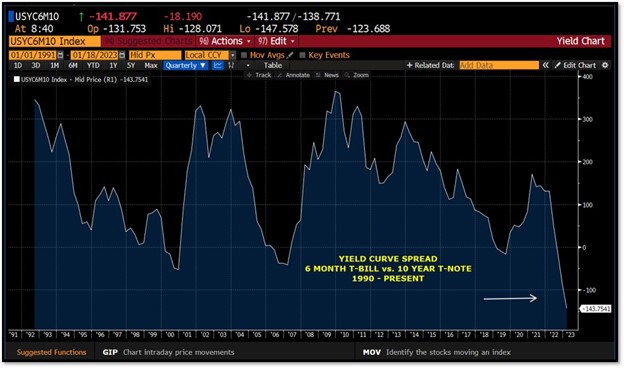

The treasury yield curve (as measured by 2 year T-Note vs. 10 year T-Note) remains inverted by near 70 basis points. The 10 year treasury note is inverted to the 6 month treasury bill by near 140 basis points with 6 month T-Bills still yielding near 4.80%. This is the most significant inversion since the early 1990’s surpassing the inversion from the 1990’s “tech wreck” recession as well as surpassing the inversion from the Financial Crisis recession. This would suggest that a significant event will cause the current inversion to reverse course. One possibility could be a much deeper recession causing the FED to reverse course quickly by cutting rates aggressively thereby bringing short-term rates back down sharply. There is precedent for this based on previous rate hiking cycles (reference the 2nd chart below). That is not my base case at present albeit I do believe we’ve seen the highs in longer-term yields.

5 year non-callable FDIC insured CD’s that as recently as October 2022 could have been purchased at yields near 4.75% are now priced around 3.75%. CD’s that are “callable” can still be purchased near 4.40%, however, with the current higher coupon rates if rates were to decline a year or so from now those CD’s would very likely be called and the investor would be forced to reinvest at lower rates.

Because the municipal bond yield curve remains positively sloped, even with the recent higher prices/lower yields I remain upbeat when it comes to prospects for the tax-exempt market this year.

The next FED meeting will be at the beginning of February with the policy announcement occurring on February 1st. Consensus as of this writing is for a 25 basis point increase taking the Federal Funds target rate to 4.75%. Given recent weakening economic data and falling inflation, if Chairman Powell makes any reference during the press conference to the idea they may soon be done with rate hikes I would expect short rates to decline with perhaps the biggest impact to 2 year treasuries as we transition from rate hikes to no more rate hikes and then to possible rate cuts.

Please don’t hesitate to let me know if you have any questions or comments.